As an aunt, you want to find the perfect gift for your niece.

You want something she will enjoy and be excited about. But you may also want to find a gift that will have meaning to her for years to come. A gift that will make her think of you and the memories you made together.

There are plenty of gift ideas to choose from. But when you choose an investment gift, you can give something that will have emotional meaning now, and real financial impact later.

In this article, you’ll learn everything you need to know about giving a financial gift to invest in your niece’s future.

{{cta-1}}

Finding the Perfect Gift Idea For Your Niece

As an aunt, you play an important role in your niece’s life. You often find yourself filling many shoes at once, including role model, friend, mentor, and more.

There are likely many occasions throughout the year where you find yourself shopping for a thoughtful gift for your niece. Whether it’s a Christmas gift, birthday gift, graduation gift, or any other special occasion, you want to find just the right thing.

You’ve probably found yourself weighing the pros and cons of a physical gift (such as toys, books, jewelry, etc.) versus a financial gift.

A physical gift is probably more exciting for a kid, especially when they’re young. The joy of a child unwrapping a gift is unmatched. But we can all admit that the joy is usually short-lived before they’re onto the next exciting thing.

With a financial gift, you can make even more of an impact on your niece’s life. Not only is a financial gift meaningful today, but it can make an incredible difference toward her future goals.

How to Make a Financial Gift to Your Niece

When it comes to making a financial gift to a child in your life, there are so many options.

Certainly, the easiest option is to put cash into an envelope and let the family decide the next steps. But there are other options where your money could have an even greater impact.

Cash vs. Investment

The first big decision to make when it comes to financial gift giving is whether to give cash or contribute to an investment account for your niece.

Both options obviously have their advantages. When you give cash, it’s a gift your niece can use right away. This is especially appealing when she’s older and has more items she wants to buy.

The other option is to contribute to an investment account for your niece. While it doesn’t seem as impactful at the time, it actually goes a lot further than just a cash gift.

Your money has a chance to grow and compound over time and your gift could be worth several times its original amount by the time your niece is a young adult.

Options for investment gifts

If you decide an investment is the right gift, it’s time to choose the best type.

One of the best ways to invest for your niece is through a custodial brokerage account such as an UGMA (Uniform Gifts to Minors Act) account. Any adult can open an UGMA account for a child in their lives.

Throughout the child’s life, you can make financial contributions, invest them, and watch the value grow. Then, when the child reaches adulthood, they take control of the account and can use it to fund any of their big goals.

As the child’s aunt, you can open the account on her behalf. You can also encourage her parents to open an UGMA account, where all of the child’s loved ones can then contribute.

Sure, there are other options you could use to invest for your niece. 529 plans are popular, as they’re specifically designed to save for a child’s college education. Many people also open a custodial IRA, which they use to get a head-start on saving for a child’s retirement.

But the thing both of these accounts lack is flexibility. Both are designed for a specific purpose. If your niece’s goals look different than you expect them to be when she’s young, she can’t easily use the money for what she truly wants.

Why choose an UGMA with EarlyBird

EarlyBird offers a simple yet innovative way for families to come together and collectively invest in a child’s future.

A parent or any loved one can open an UGMA account with EarlyBird and start saving for a child’s future.

The account custodian (the person managing it until the child comes of age) can choose from one of five ETF portfolios ranging from conservative to aggressive.

They can also invest up to 5% of the portfolio into values-based funds made up of companies that support causes that your family and the beneficiary (in this case, your niece) believe in.

Once the account is set up, the custodian can invite other loved ones to join, and they can contribute however much or often as they wish.

EarlyBird makes your contributions even more special by allowing contributors to leave a short video message, which will serve as a meaningful, personalized gift for your niece.

The Impact of a Financial Gift

Here are four reasons why a financial gift can be the perfect present for your niece.

Your niece can reach her future goals

Chances are, your niece will have many big expenses ahead of her in her early adult years.

Many young people decide to go to college, which costs tens of thousands of dollars (and can easily exceed $100,000). But she may also dream of starting her own business, traveling the world, or starting a family.

Your financial gifts can help your niece reach those big goals, whatever they may be.

Your niece will develop financial literacy

Financial literacy is unfortunately lacking today.

Data from the FINRA Foundation found that basic financial literacy has declined over the past decade, and young Americans have seen the greatest declines.

Unfortunately, since financial concepts often aren’t taught in schools, it’s up to families to make sure that children are prepared.

By contributing to an investment account for your niece — and more importantly, involving her in the conversation — you can help open her eyes to how finances work and teach her the importance of saving and investing for the future.

Your niece can take ownership of her future

One of the most important characteristics of a custodial brokerage account is that the funds in the account truly belong to the child.

When you contribute to one of these accounts for your niece, the money legally belongs to her, and she’ll take control of it when she reaches adulthood.

While this distinction might not seem important, it really is.

Throughout your niece’s life, you can talk to her about the money in the account, and encourage her to set big goals for what she’ll do with it. By the time she reaches adulthood, she’ll feel a sense of ownership over the funds, and they’ll mean that much more to her.

How compound interest helps your gift grow

Any financial gift will make a difference in your niece’s life. But thanks to compound interest, an investment gift can be even more impactful.

When money sits in an investment account, it compounds. This means that any returns your money earns are added to the principal and also begin to earn money.

Let’s say that each year for your niece’s birthday gift, you put $100 into a bank account that doesn’t earn any interest. When she reaches 18 years old, the account would have $1,800 in it.

But, what if you had instead put that money into an investment account?

Let’s say the money saw an annual return of 10% (which is the average stock market return, according to the Securities and Exchange Commission). When your niece turns 18, the account could hold more than $5,000.

What to Know About Financial Gifts

Before you open an UGMA account for your niece, there are a few things you need to know.

Gift taxes

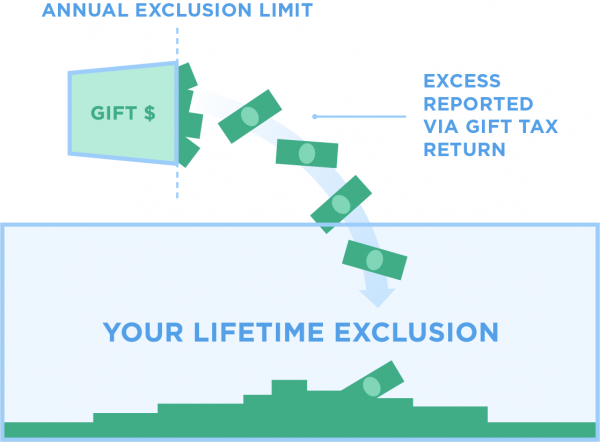

The federal government imposes a tax on gifts over a certain amount. Most families will never have to worry about the gift tax, but it’s important to know about it nonetheless.

Anytime you gift $15,000 or more to another person in a single year, the IRS requires that you fill out a gift tax return. But don’t worry — that doesn’t necessarily mean you’ll pay gift taxes.

The IRS also allows a lifetime exclusion: an amount people can gift throughout their lives before they must pay gift taxes.

As of 2021, the lifetime exclusion is $11.7M. As long as you give less than this amount over your lifetime, you won’t pay gift taxes when you contribute to your niece’s UGMA account.

Taxes on earnings

In general, the IRS requires people to pay taxes anytime they earn money. This expectation also applies to a child’s unearned income, such as through a custodial brokerage account.

There are a couple of tax perks to building wealth for a child through an UGMA account.

First, the IRS doesn’t collect taxes on the first $1,100 of a child’s unearned income. The next $1,100 is taxed at the child’s tax rate, which is usually lower than that of an adult custodian.

It’s not until a child earns $2,200 or more in a year that the money is taxed at the parents’ tax rate.

Custodian

Every custodial brokerage account has a custodian, who is the adult that opens and manages the account. The custodian makes all of the investment decisions related to the account throughout the young person’s childhood.

The custodian of an UGMA account is often the parents, but it doesn’t necessarily have to be. Another adult in the child’s life could open an UGMA account on their behalf.

As a child’s aunt, you could encourage your family to open an UGMA for their child so you can contribute to it. But you can also open the account yourself, leaving you in control of all investment decisions.

Investment options

One of the benefits of an UGMA account is the wide range of investment options. These accounts can hold many different types of financial assets, including stocks, bonds, funds, insurance policies, annuities, and cash.

It’s important to note that UGMA accounts generally can’t hold high-risk or speculative investments such as stock options and futures.

EarlyBird is the perfect choice for families who don’t want to hand-pick individual stocks or funds for an UGMA account. Custodians are offered a list of five ETF portfolios, so everyone will be able to find one that suits their needs, without having to be a professional investor.

Account ownership

One of the most important things to know about custodial brokerage accounts is that no matter who the custodian is, the money or assets in the account legally belong to the child. There are a couple of consequences to this.

First, any gift to the custodial account is considered irrevocable — you can’t take it back. In most cases, the custodian can’t even remove money from the account.

There are rare occasions where money can be taken from the account for the benefit of the child. But even in these cases, the money can’t be used for the typical costs associated with raising a child.

Then, once the child reaches either 18 or 21 (depending on the state), they take control of the UGMA account and all of the assets within.

This means that when you gift money into your niece’s custodial account, you know that she’ll receive the money. Her parents can’t use it for another purpose, and she’ll be free to use the money to fund anything she wants.

This is an important consideration for families using an UGMA account to specifically save for a child’s education expenses. While you might hope or expect that they’ll use the money to pay for college, they don’t have to. Once they reach adulthood, they can use that money for any purpose.

As an aunt, you might see this as a benefit. But, it highlights the importance of teaching your niece financial literacy as her investments grow. So that you and her family can be confident she’ll make smart decisions with her money when the time comes.

Conclusion

A financial gift from you to your niece is one of the best ways you can show you that you love her today, while still making a meaningful investment in her future.

There are plenty of investment accounts specifically designed for young people, but an UGMA with EarlyBird is an easy way for all of the people in a child’s life to come together and support their future goals.

By making a contribution to your niece’s EarlyBird account, you’ll leave a lasting impact with your dollars and an emotional impact with your video message.

Download EarlyBird on the app store today to start investing in the kids you love.

{{cta-1}}

This page contains general information and does not contain financial advice. All investments involve risk. Any hypothetical performance shown is for illustrative purposes only. Actual investment performance may be different for many reasons, including, but not limited to, market fluctuations, time horizon, taxes, and fees. Please consult a qualified financial advisor and/or tax professional for investment guidance.